Detroit housing loss prevention program yields 85% homeownership rate four years later

Contacts: Lauren Slagter, lslag@umich.edu; Nardy Baeza Bickel nbbickel@umich.edu

DETROIT – A program designed to help tenants in Detroit to purchase their homes helped 85% of participants sustain homeownership for four years, an important milestone as owners may start to see the wealth-building benefits and other advantages of homeownership after at least five years of ownership.

The findings from an evaluation of the Make It Home program by the University of Michigan also offers recommendations for sustaining homeownership among more households with low incomes, such as providing financial counseling, a home inspection prior to purchasing the home and financial help for major repairs, if needed.

“The study underscores the importance of affordability and housing that is in good condition to promote stability among people with low incomes,” said Roshanak Mehdipanah, an associate professor of health behavior and health education at U-M’s School of Public Health and co-author of the Make It Home evaluation. “It was the tenants who didn’t have any path to homeownership who saw the most instability.”

The U-M analysis focused on the first year of the Make It Home program’s implementation in 2017 when the City of Detroit used the Right of First Refusal to help 80 Detroit renters to purchase their homes. People in the program lived in properties experiencing tax foreclosure, meaning the property owner had failed to pay property taxes for at least three years.

The City of Detroit used donated funds from Rocket Community Fund (formerly Quicken Loans Community Fund) to purchase tax-foreclosed homes from the Wayne County Treasurer and transferred them to United Community Housing Coalition.

UCHC then sold the properties to tenants with quit claim deeds or on 0% interest land contracts, an alternative to mortgage lending that allows prospective buyers to make monthly payments toward homeownership.

Since its start, Make It Home has helped nearly 1,200 households in Detroit avoid housing loss by giving them the opportunity to purchase the properties where they live.

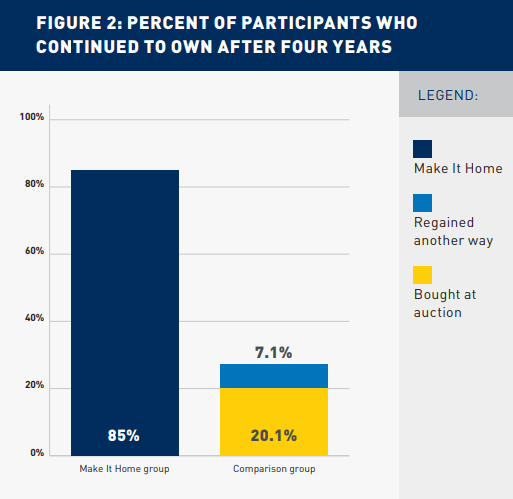

By the end of the first year of the program, 81% of Make It Home’s initial 80 participants (65) owned their homes outright or continued to hold a land contract. In the four years following the properties’ tax foreclosure in 2017, Make It Home resulted in sustained homeownership for 85% of participants. The median household size for the initial Make it Home group was three people, and 89% of participants made less than $37,080 a year.

“The Make It Home program set out with two main goals: to prevent tenants from losing their housing in the crisis of a landlord’s tax foreclosure and to help them sustain their homeownership. Our evaluation found the program accomplished those goals for 85% of its first group of participants,” said Margaret Dewar, professor emerita of urban and regional planning at U-M and co-author of the evaluation of the Make It Home program.

To compare results, researchers also studied outcomes for 154 households with similar characteristics that UCHC attempted to help buy at the county 2017 tax auction. In that group, only 27% sustained homeownership four years later, 109 had their homes sold at auction, and 15% of those tenants experienced eviction within the next four years.

Of the original Make it Home group, six households that successfully purchased their houses went on to sell them after less than four years of ownership. But even those homeowners said they were glad to have been able to buy their houses and wanted to stay despite the hardships they had encountered, according to the researchers.

One participant said Make It Home reduced the “bad feeling [of] not having a place to stay,” while another said the program provided the opportunity to “save the home” where the household had been living for a long time. Participants spoke about the “ease” of acquiring their home because of the support provided by UCHC. For some, homeownership had seemed unattainable prior to this process.

The researchers said numerous factors threaten the continued homeownership by program’s participants. More than 30% of Make It Home purchasers faced imminent foreclosure for failure to pay property taxes. Two homeowners left their houses vacant. Owners cited hardships with poor condition of the houses, high housing-related expenses, and loss of income during the COVID-19 pandemic.

“People said they sold their houses because they couldn’t keep up with repairs and the lack of upkeep was presenting health hazards. They sold because a loved one had died, a relationship ended, or an investor harassed them into selling the house. Housing instability compounds the stress of navigating these life crises,” Dewar said.

The researchers recommend ways to improve sustained homeownership rates for buyers with low incomes, including:

- Provide pre-purchase homeowner education and financial counseling to help people build the financial stability needed to purchase and continue to own a house;

- Inspect houses prior to purchase, so prospective buyers have a clear understanding of the scale of needed repairs;

- Increase home insurance awareness and access, as land contracts do not require the buyer to carry home insurance and out-of-pocket repair costs can be expensive;

- Provide financial help for major housing repairs to people who cannot obtain a conventional home repair loan or equity line of credit due to low credit scores, lack of equity in a property, or lack of disposable income for loan payments; and

- Make post-purchase support like utility payment plans and property tax relief available to deal with ongoing housing costs and prevent loss of housing.

“Additional support services would help ensure homeowners receive the benefits of longer-term homeownership. In Detroit, assistance in enrolling in programs that reduce property taxes is vital because tax delinquency can quickly lead to loss of a home,” Mehdipanah said. “By monitoring efforts like the Make It Home program over time, we gain new insights into the challenges facing homeowners and the types of support that would make a difference.”

RELATED

- 9 in 10 Detroit eviction cases filed during pandemic came from landlords not compliant with rental codes

- U-M study on Detroit’s Make It Home Repair Program links home repairs, housing stability

- New land contract buyer guide assists Detroiters on path toward homeownership

Interested in more Poverty Solutions news? Sign up for our newsletters >